{kind=link}

The HDFC Multicurrency Forex Card is designed to be a convenient travel companion for frequent international travellers. Designed to hold multiple foreign currencies in a single card, it eliminates the hassle of carrying cash or managing multiple currency wallets.

With zero forex markup for same-currency transactions and wide global acceptance, this prepaid travel card is a cost-effective alternative to using a typical debit or credit cards abroad.

In this review, we’ll dive into its features, fees, and whether it’s the right choice for your travel needs.

Fees & Charges

| Type | Prepaid Forex Card |

| Issuance Fee | 500 INR + GST |

| Reload Fee | 75 INR + GST |

| Currency Supported | – Multi-Currency Wallet – Supports 22 Currencies |

| Usage | – POS / Contactless – ATM – Online |

| Forex Markup Charges (For Load/Re-load) |

~2.5% (Bank says no charges) |

| Cross currency markup Charges | – 2% (wallet to wallet transfer) – 2% (when funds low on one wallet) |

| Daily ATM withdrawal Limit | USD 5,000 (or equivalent) |

| TCS | – Nil upto 7L per FY – 20% beyond 7L per FY (purpose: personal spends) |

| Reload Method | User friendly, via Online Portal |

How it works?

The HDFC Multicurrency ForexPlus Card lets you load multiple currencies onto a single card, acting like a digital wallet for hassle-free international spends.

You can load and reload funds as needed, making it a flexible option for frequent travellers. Here’s a nice video by the bank on how the card works.

While HDFC markets this card as having 0% forex charges, it’s important to note that a ~2.4% markup is already applied at the time of loading.

So, while you avoid transaction fees on same-currency spends, the conversion cost is built into the exchange rate. Here’s a deeper look at how it works.

Hands on Experience

I’ve mentioned hidden charges on load/reload before – back when I first wrote this article ~8 years ago.

But recently, I got the HDFC Multicurrency Forex Card myself, and here’s a live example of the actual difference in charges today:

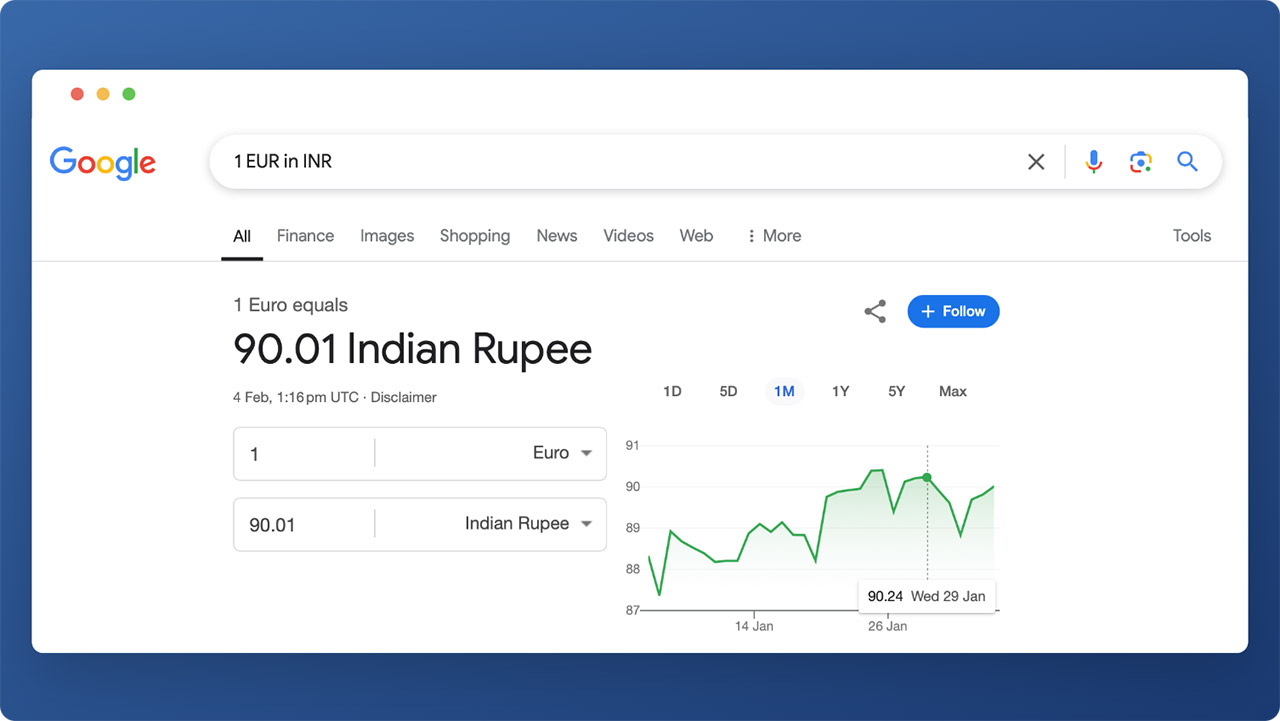

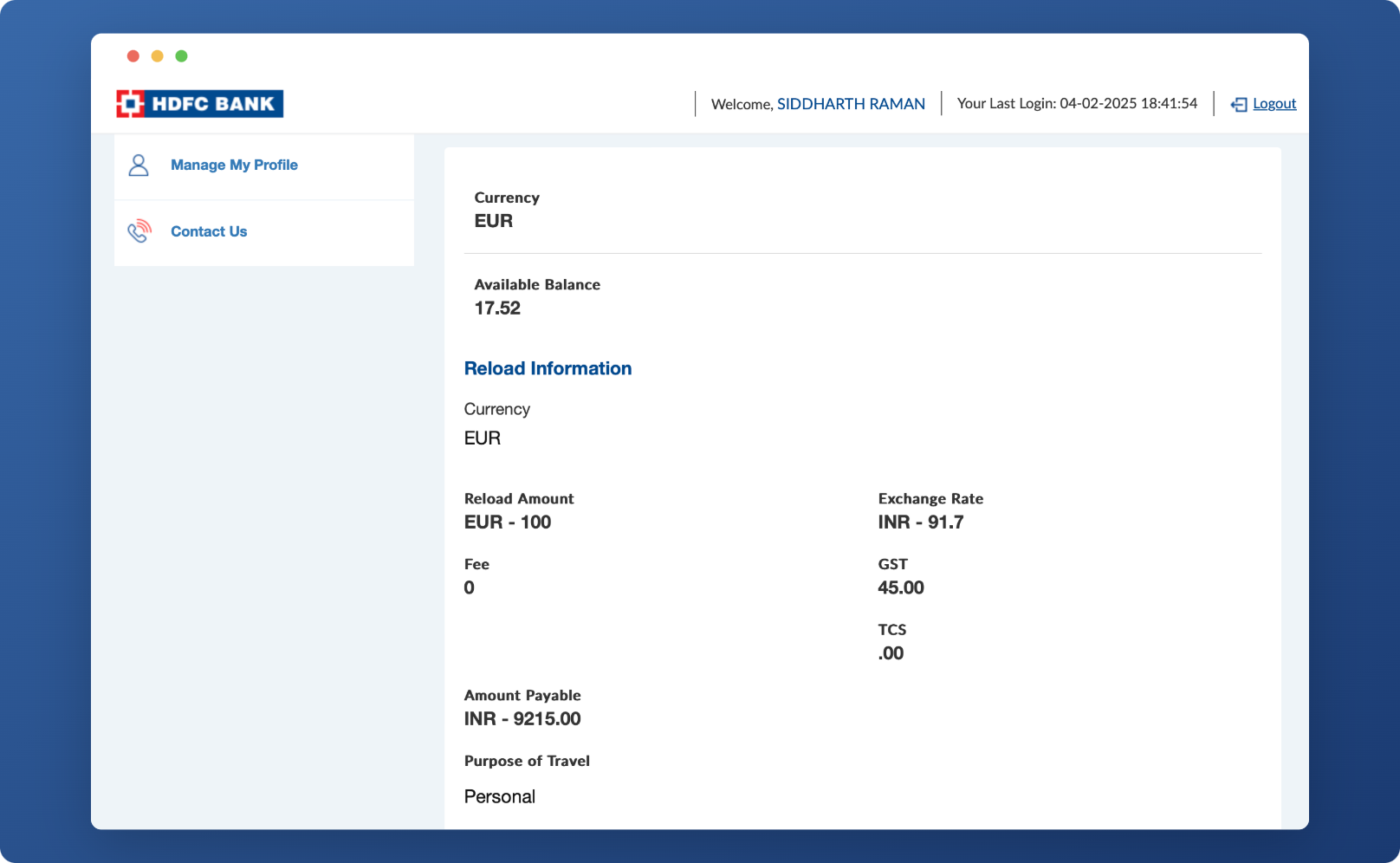

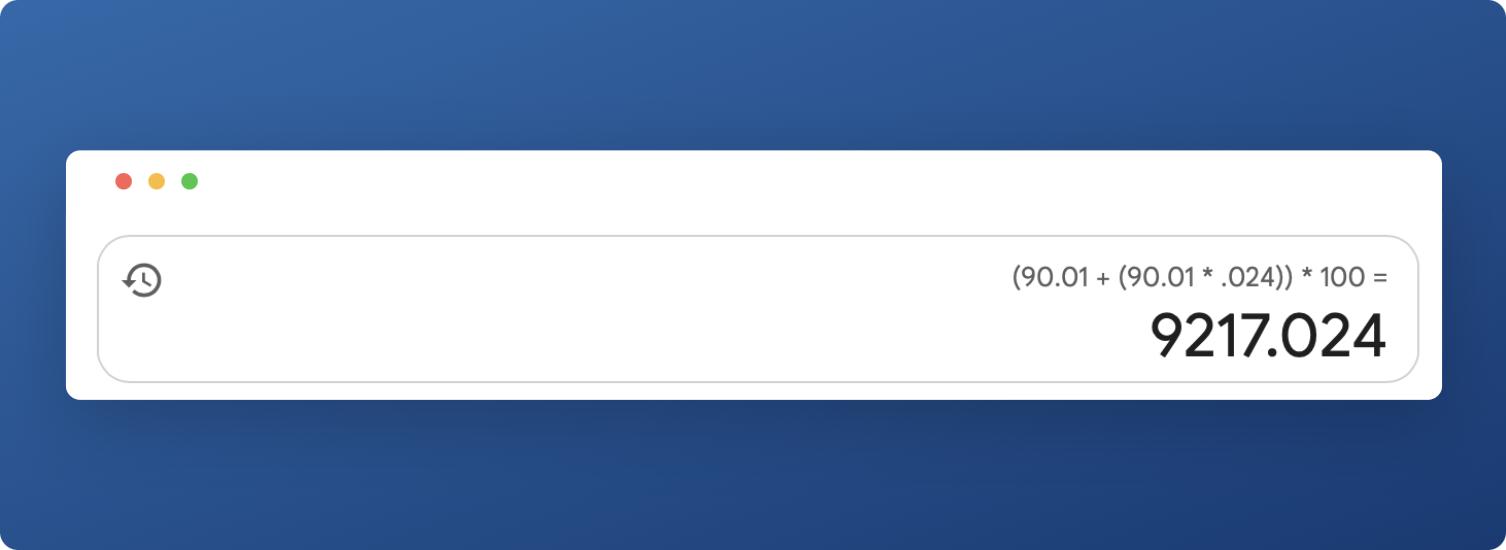

- 1 EUR in INR (as on google.com): 90.01 INR

- 1 EUR in INR (HDFC rate): 91.7 INR

- Difference along with charges: ~2.4% (hidden markup fee)

That’s roughly a 2.4% markup fee – nowhere mentioned by the bank – but in line with the lowest forex markup on HDFC’s super-premium credit cards like Infinia.

However, keep in mind that the HDFC Multicurrency Forex Card can be an expensive choice if you’re traveling to a country where the local currency isn’t supported.

In that case, you’ll get hit with markup fees twice – once while loading the card and again while spending.

5X/10X Rewards

The HDFC Forex Card gained popularity between 2016-2018, thanks to lucrative reload offers on HDFC Bank credit cards – including 1% cashback, 5X rewards, and even 10X rewards.

However, these offers stopped for nearly five years. Now, in 2025, HDFC has finally brought them back.

A 5X rewards promo on forex reloads is currently active (Jan-March 2025), here’s link to t&c. Since it hasn’t been widely tested yet, it’s best to load a small amount first and check for rewards in the first week of next month before going all in.

While that’s good, it is to be noted that I did not even receive 1X points on my test load of 100 EUR when the offer was not live.

Should you take it?

It depends on the needs. For most, 0% forex debit cards like IndusInd Pioneer or IndusInd Exclusive debit cards are sufficient.

But If there are reload offers like 5X rewards, it does make sense to go for it even though the bank charges ~2.4% fee, as it will still result in net gain.

On other side, if you hold HDFC Infinia and has only POS spends and don’t require Cash withdrawal option, you’re better off with the Infinia Credit Card with Global Value Program enabled so that you’ll not only get 3.3% rewards but also additional 1% cashback on the spends.

Bottomline

The HDFC Multicurrency Forex Card is easy to apply for, load, and use, but it comes with hidden charges that aren’t explicitly mentioned by the bank. That said, it’s still a decent option if you’re visiting only a few select countries.

However, if you travel to multiple countries frequently, a 0% forex debit card is a much better choice – eliminating complex calculations and double markup fees. Simply withdraw local currency from any bank ATM abroad, just like I’ve been doing for the past eight years.

Personally, I used to rely on the IndusInd Exclusive Debit Card, but I’ve now switched to the IndusInd Pioneer Debit Card – both of which have zero charges on forex transactions, including markup and ATM withdrawals. This makes my travels completely cashless, hassle-free, and cost-effective.

What’s your experience with Forex Cards? Feel free to share your thoughts in the comments below!