{kind=link}

Health insurance and the claims process often remain a grey area for many – not just in India, but across the globe. Despite its importance, most people I’ve spoken to, like friends & family don’t seems to have enough trust on insurance companies.

There’s a widespread perception that claims are complicated, difficult to navigate or are often rejected without clear reasons.

Recently, I had to go through the process myself – a health insurance reimbursement claim and I’m happy to share that the entire claim was settled for 100% of the billed amount.

In this article, I’ll walk you through my end-to-end experience with ICICI Lombard Health Insurance, specifically under a policy issued through American Express India.

Whether you’re preparing to make a claim, or simply want to understand how the system works, this should give you a clear picture of what to expect and how to improve your chances of a smooth, successful outcome.

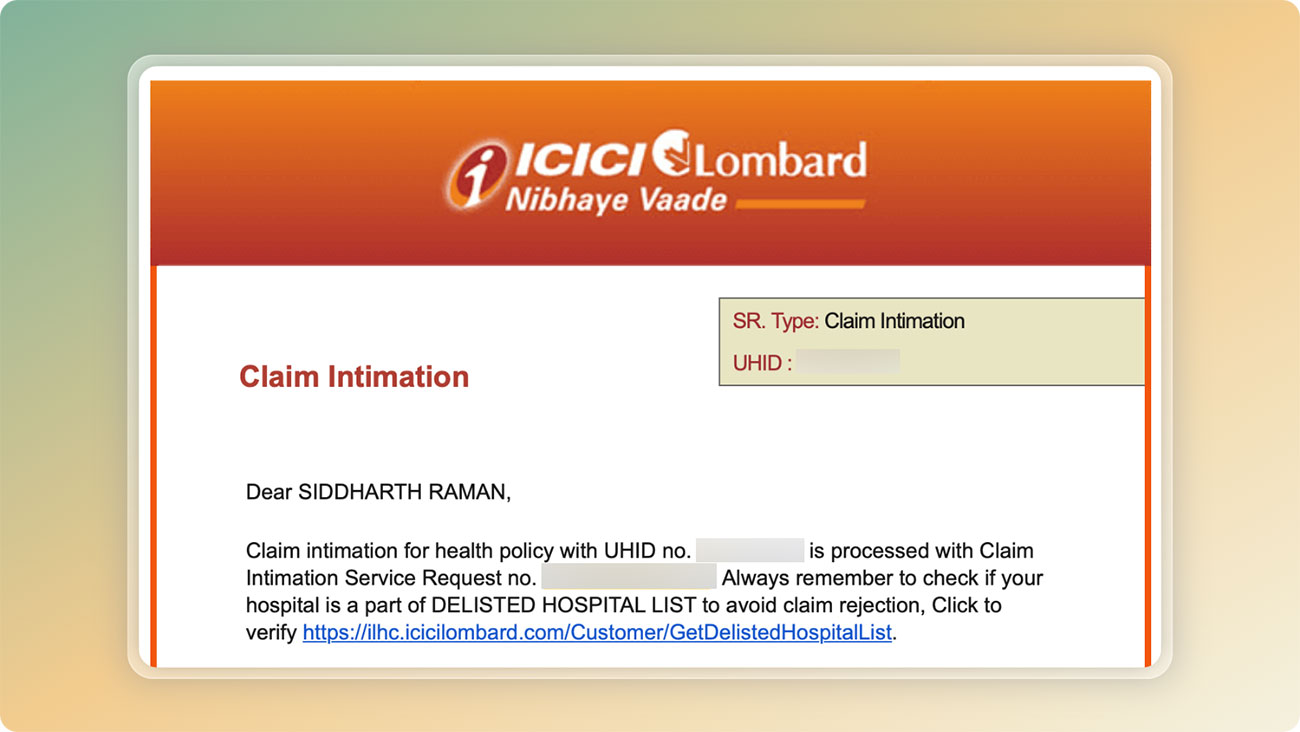

Step 1: Intimation

I called the dedicated ICICI Lombard helpline for American Express cardholders and informed them of my planned hospital admission, including the admission date. This triggered an email confirmation as above.

I also requested for further written confirmation, as the treatment falls under the AYUSH category. The confirmation email was then received accordingly.

Step 2: Admission & Papers

I then got admitted for the treatment and collected all the papers that might be required.

As it’s going to be a re-imbursement claim, I made sure I’ve all necessary documents in order. This included invoices, payment receipts, proof of payments, consultation papers, test reports, and related documents.

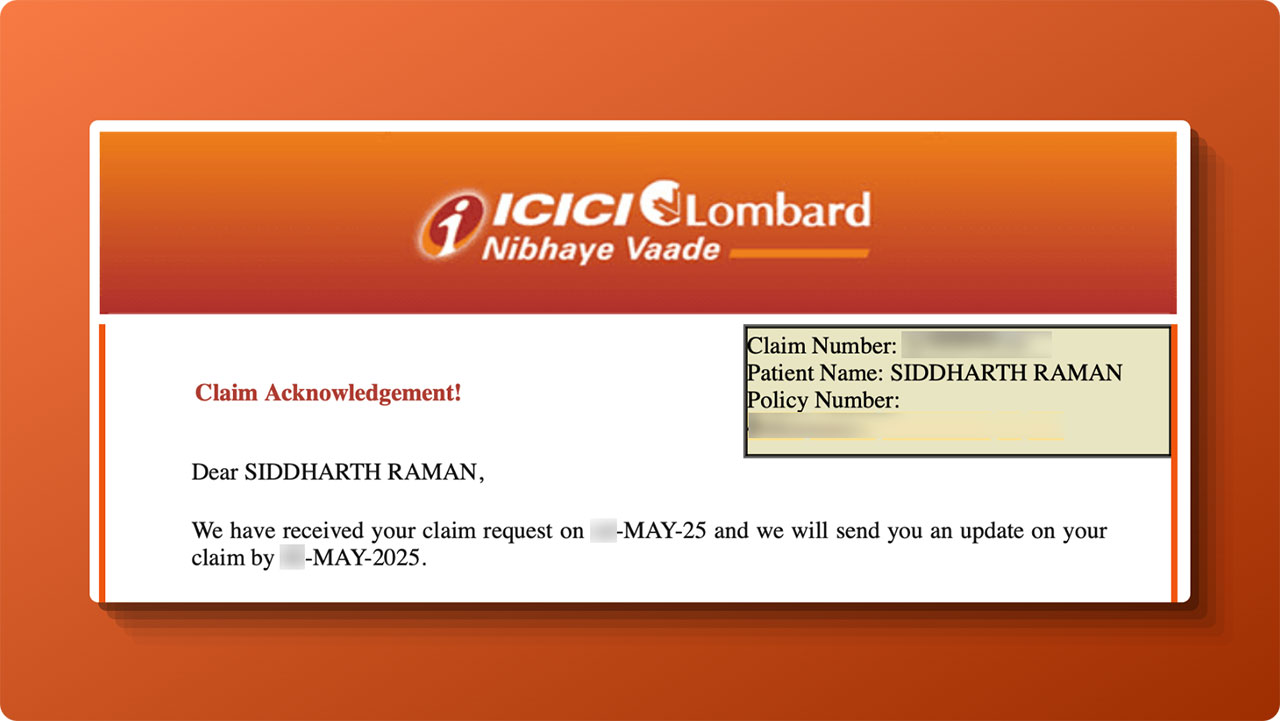

Step 3: Claim Submission

Fortunately, ICICI Lombard has an excellent system in place to initiate claims digitally through its mobile app, ILTakeCare.

Day 1: I filled in the required details and uploaded every relevant document I could think of, thanks to thorough prior research.

The overall submission process was smooth, and I received a temporary claim number. A day later, the claim was accepted for further processing, and I was issued a final claim number.

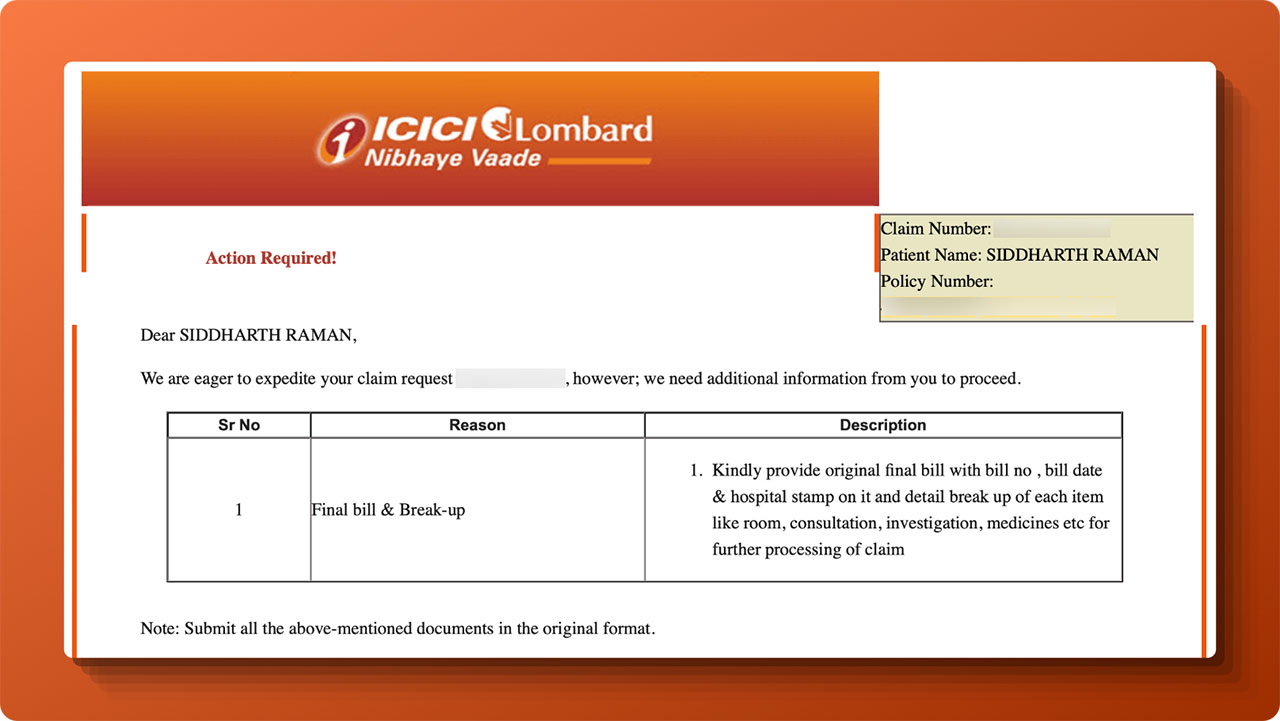

Step 4: Additional Docs Requested

Day 6: I received an email from ICICI Lombard requesting additional documents along with a signed consent letter. This was weird, because the required documents were already uploaded.

Day 11: Another request came in for more documents. I had to contact the hospital again to obtain the required paperwork, which I then uploaded.

At this point, the process started to feel frustrating, so I escalated the issue to both the Amex Insurance team and the ICICI Lombard Grievance team.

The Amex team simply advised me to follow the standard process: so the expectation of support from their end didn’t materialize.

On the other hand, the ICICI Lombard grievance team called back within a day, assuring me that they were looking into the matter.

Step 5: Field Verification

A few days after submitting all documents and escalating the case, I received a call from someone claiming to be from ICICI Lombard’s field verification team.

He mentioned that he needed physical copies of the documents and required a filled questionnaire form.

Unfortunately, I was in Switzerland by then, so I explained my situation.

He checked with his superior and confirmed that digital copies would suffice, but the form had to be filled in person. He suggested that a family member could do it on my behalf, along with their ID proof.

I asked my dad to complete the lengthy questionnaire, which asked for detailed information on my medical history, previous related OPD consultations (with supporting documents), my work profile, and more.

Luckily, I had all my documents stored on the cloud, so handling these requests didn’t take any extra time.

The next day, he called again to ask about my mode of transport to the hospital and requested proof. I had my flight tickets ready and promptly shared them.

Initially, I had wondered how a claim could be assessed with such limited input during submission, so it made sense that they’d follow up with these queries later.

While that’s fine, I wish they asked for everything upfront instead of initiating a separate field verification process. But that’s just how it works!

That said, the field executive was extremely polite throughout, and I was relieved that they didn’t insist me to fly back to India just to prove I exist, lol.

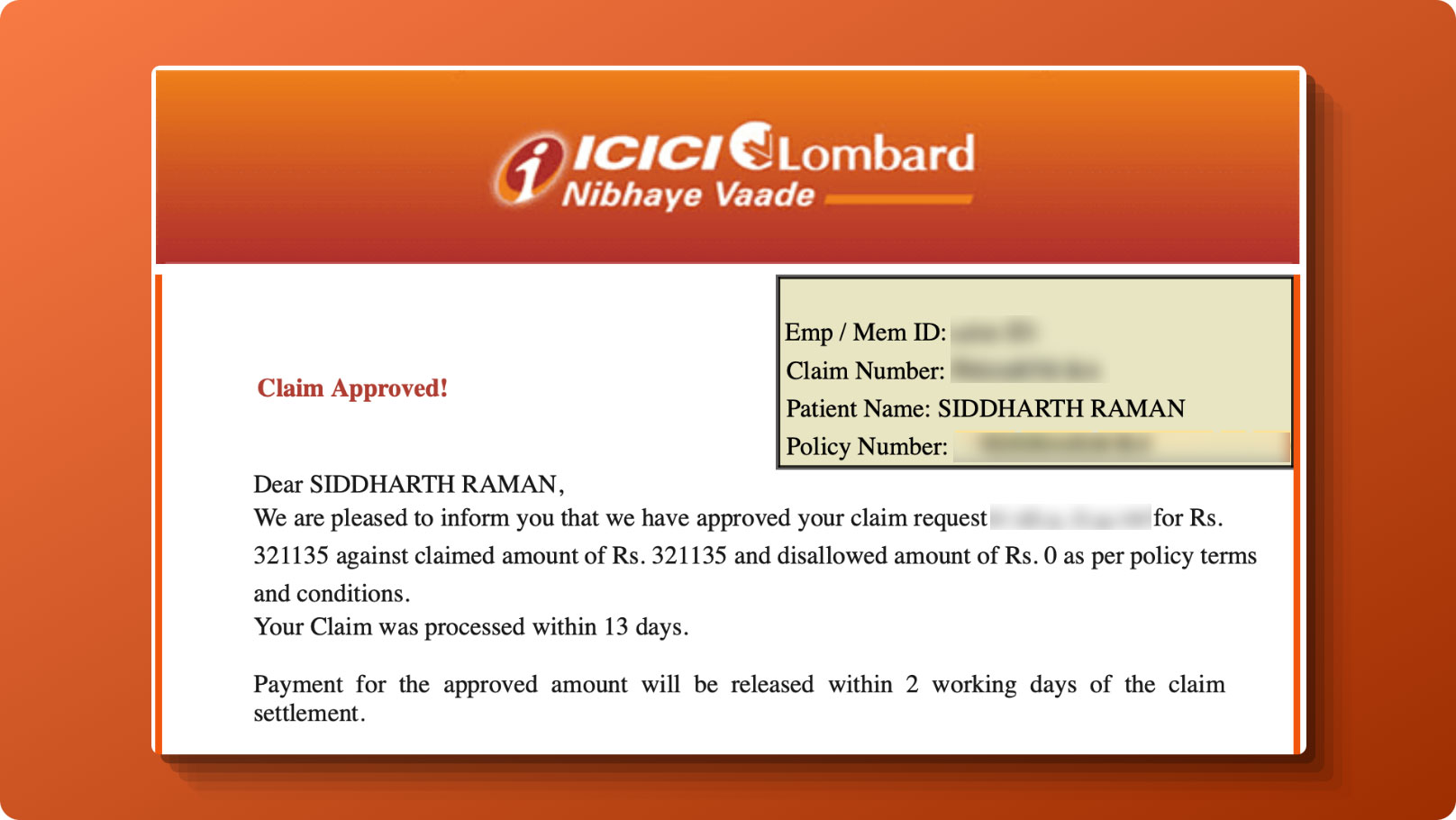

Claim Approved

Day 22: Within a day of submitting the flight tickets, the claim was approved for 100% of the billed amount, and I received an email confirmation the very next day.

The email mentioned that the payment would be initiated within two days and in fact, it was credited within just one day.

It’s worth noting that the 100% approval was likely due to the “Claim Protector” add-on cover. Without it, a partial deduction might have been applied. This add-on is quite important, yet many people tend to skip it, and that can be an expensive mistake.

For example, a friend of mine recently needed to use his health insurance but ended up not filing a reimbursement claim because the deductibles were so high that he felt it doesn’t make sense to go through the whole process anyway.

In-fact I also have an additional add-on called “convalescence benefit” (10K INR) which I just realised a day back that I’m yet to claim. I was told prior that these extra add-on benefits along with pre/post hospitalisation expenses can be claimed once the main claim goes through.

And apart from that, I do have an additional OPD cover and if you were reading the blog for sometime, you might have gone through my OPD claim experience in the past.

Hence, investing a little extra in the right add-ons can make a big difference when it actually matters.

So overall it took about 22 days for the complete reimbursement claim process, end-to-end.

Key Takeaway

During the whole process, I spent a good amount of time researching on the best practices to make sure the claim doesn’t get delayed or rejected. So here are some key points worth knowing:

- Buy policies through premium channels such as Amex or premium banking services, as these are generally viewed as lower-risk by insurers.

- Claims made after the moratorium period, typically after 5 consecutive years are usually considered safer and more straightforward.

- Maintain a complete and accessible medical history as having past OPD records and lab reports ready can make a big difference.

- Stay alert to emails and SMS notifications so you can respond promptly to any document or clarification requests.

- Be available in person whenever possible as higher claim amounts may trigger field verification, which often requires in-person involvement.

This much should suffice for reimbursement claims. The process is, of course, much easier if the claim is cashless.

While my experience is with ICICI Lombard, the overall claim process should be broadly similar across most major insurers.

That said, this doesn’t necessarily mean ICICI Lombard is the best option — health insurance is a complex product, and what’s suitable depends on factors like the type of coverage you need, age, and medical history.

For example, I’ve insured my parents under Niva Bupa since ICICI Lombard via Amex doesn’t support policy porting. Porting would have meant losing their existing insurance no-claim history (as it supports moratorium period), which wasn’t a risk worth taking.

In a nutshell

Health insurance reimbursement claims may seem complex, but with the right preparation and awareness, the process can be smoother than expected. My experience with ICICI Lombard under a policy issued via AmEx India was largely positive, ending with a 100% settlement.

While the field verification process added a few extra steps, being proactive and having digital backups helped speed things up.

Although the claim process could be more transparent, especially with upfront documentation requirements, it’s reassuring to know that a well-documented and eligible claim does get honoured.

Have you made any health insurance claim for you or your family? Feel free to share your experiences in the comments below.